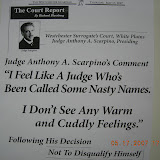

- Westchester Surrogate Judge Anthony A. Scarpino OK with Convicted Felon as Trust Fiduciary

- Judge Scarpino ignores any conflict as he used to work for the same Convicted Felon- Banker's Trust Company

- Scarpino, Pfau, Spatz and OCA continue to ignore fraudulent Letters Testamentary

Matter of Estate of Ralph P. Manny

WESTCHESTER COUNTY - Trusts and Estates

New York Law Journal - June 4, 2010

WESTCHESTER COUNTY - Trusts and Estates

New York Law Journal - June 4, 2010

Surrogate Scarpino - PETITIONERS filed the instant proceeding to judicially settle their intermediate account as co-trustees of an irrevocable inter vivos trust established by decedent for the benefit of his great-grandchildren and their issue. Objectants alleged petitioner co-trustees should be surcharged and/or forfeit any commissions they retained for the years in which they did not provide annual statements in compliance with Surrogate's Court Procedure Act §2309(4) and §2312(6). The court stated that even though it had the discretion to disregard minor deviations from the statutory requirements, petitioner co-trustees' complete failure to provide any great-grandchild and his/her parents with the required annual statements for a 20-year period cannot be considered a minor deviation. Therefore, the court ruled that petitioner co-trustees must pay the trust statutory interest, 9 percent per annum, on the commissions improperly taken in 1977, 1978, and from 1982 through 1997.

Decision of Interest

Published in the New York Law Journal 6/4/2010

Matter of Estate of Ralph P. Manny, 1992-1319/B_Decided: May 20, 2010

Surrogate Anthony A. Scarpino

WESTCHESTER COUNTY - Surrogate’s Court

Bleakley Platt, & Schmidt represented: Petitioner - Deutsche Bank AG, New York (formerly Bankers Trust Co.);, Feinstein & Naishtut represented: Objectant — David M. Place. --- Robert L. Byrne, Esq. represented: Objectants — Lauren C. O'Brien, Chrystie O'Brien, John W. Young, Brittany Young, and Zachary H. Place. --- Stephen O'Brien — Objectant, acting Pro Se; and Anne Penachio, Esq. — Guardian Ad Litem for all Infant Great-Grandchildren and Great-Great-Grandchildren of Ralph P. Manny

DECISION AFTER TRIAL

This is a contested proceeding commenced by Deutsche Bank AG, New York (f/k/a Bankers Trust Company ["the Bank"]) and James F. Downey ("Downey" [collectively "petitioners"]) to judicially settle the first intermediate account of the co-trustees of an irrevocable inter vivos trust established by Ralph P. Manny ("decedent") for the benefit of his great-grandchildren and their issue ("Trust"). From November 9 — 17, 2009, a non-jury trial occurred as to the objections filed to the account, which covers the period December 21, 1976 through March 31, 1999 ("accounting period"). The adult objectants who appeared at trial by counsel are Lauren C. O'Brien ("Lauren"), Chrystie O'Brien ("Chrystie"), John W. Young, Brittany Young ("Brittany"), Zachary H. Place, and David M. Place. Stephen O'Brien, Jr. ("Stephen"), the brother of Lauren and Chrystie (collectively "O'Brien siblings"), appeared pro se at the trial. The court also appointed a guardian ad litem ("GAL") for decedent's infant great-grandchildren and great-great-grandchildren, and she filed objections on their behalf and represented their interests at trial.

BACKGROUND

The Trusts Created for Decedent's Three Daughters and Their Issue In 1972, decedent, who died on February 12, 1993, established separate trusts for the benefit of each of his three daughters — Ella Place, Sally Cross and Ann Beck — and their respective "issue" ("Place Trust","Cross Trust" and "Beck Trust", respectively). Each trust contains virtually identical language for the benefit of each daughter's family, differing solely with respect to the identity of current, presumptive and contingent beneficiaries. Also, each trust authorizes the trustees to pay, in quarterly or other "convenient" installments, net income and/or principal, in its "absolute discretion" for the benefit of each daughter and/or her living issue. In 1991, the Bank became sole trustee of each of these trusts, and continued to serve in that capacity through the accounting period. 1

The Subject Trust

In or about August 1976, Downey, then an attorney at the law firm of Webster & Sheffield ("Webster firm"), which handled decedent's legal affairs at that time, developed the idea of creating the Trust as an estate planning tool for decedent in response to pending Congressional legislation known as the "generation-skipping" tax bill (T: 52-68, 72-76, 90-93). On December 21,1976, decedent executed the Trust (Pet. Ex. 2), appointing the Bank and Frederick Van Vechten ("VanVechten"), one of Downey's senior law partners at the Webster firm, as original co-trustees. VanVechten and the Bank served as co-trustees of the Trust until VanVechten's death on January 7, 1991. On January 18, 1991, Downey succeeded VanVechten as co-trustee (Pet. Ex. 108). Article I of the Trust provides (emphasis added): A. The Trustees shall pay, in quarterly or more frequent convenient installments, or apply to or for the benefit of such of [decedent's great-grandchildren and their issue (hereinafter called the "beneficiaries")] as are living at the time of the payment or application * * * so much of the net income as the Trustees may in their absolute discretion consider to be in the best interests of the particular beneficiaries, it being [decedent's] intention that the income need not be equally divided among them; and that the Trustees shall accumulate and add to the principal any balance of the net income not so paid or applied. Without limiting the generality of the foregoing, [decedent] recommends that the Trustees consider using some or all of such income to help defray, in appropriate cases, some of the educational costs of the beneficiaries. B. During the continuance of the [T]rust, the Trustees are authorized to pay or apply from time to time to or for the benefit of a beneficiary such amounts of the principal as the Trustees, in their absolute discretion may determine to be necessary because of an accident to, illness of, or other emergency affecting such beneficiary. Pursuant to Article I(C), the Trust will terminate upon the occurrence of the earlier of the following dates: (i) 21 years after the death of the last surviving grandchild who was living at the time the Trust was created; or (ii) when the last great-grandchild attains the age of 21 — currently projected for 2026. Upon its termination, the Trust's remaining principal must be paid equally to all living great-grandchildren and to the then-living issue of any deceased great-grandchild per stirpes (Pet. Ex. 2; T: 366-369). Also, Article II(B) entitles the trustees to "deduct and retain without court approval" such commissions as may be "allowed from time to time" under applicable New York law.

Decedent's Great-Grandchildren and Great-Great-Grandchildren. At the time he established the Trust, decedent had seven great-grandchildren: the three O'Brien siblings, who are grandchildren of Ella Place, as well as Eva Breneman, Reed Breneman, Aaron Kielhack and Sarah Kielhack, who are grandchildren of Sally Cross. The eldest great-grandchild — Stephen — was born in 1968. Upon decedent's death in 1993, there were 17 great-grandchildren. Currently, there are 22 great-grandchildren (four infants) and 11 great-great-grandchildren (all infants) (T: 548-549).

The Account

The Trust was funded with securities valued at $995,052.00. At the close of the accounting period, the Trust's principal had realized gains in the sum of $3,175,466.61 and realized losses in the sum of $358,814.93. Also, the principal balance on hand had an inventory value of $2,643,058.44 and a market value of $7,102,076.30. There were no distributions of principal during the accounting period (Pet. Ex. 1 — Sch. A, A-1, B, F, D). Additionally, the Trust earned income in the sum of $2,326,212.89, of which $938,898.32 was distributed to or for the benefit of 10 great-grandchildren, including the O'Brien siblings. Also, through August 1995, income totaling $531,002.20 had been accumulated and transferred to principal. Subsequent to August 1995, petitioners retained any income in an investment account they established in or around 1998 ("retained income account"), the aggregate value of which was $406,519.00 at the close of the accounting period. There were income credits of $1,917,108.99, leaving $409,103.90 as the balance of undistributed income remaining on hand (Pet. Ex. 1 — Sch. AA, A-2, C-2, D-1, F).

As to income distributions during the accounting period, in 1977 and 1978, upon learning of financial difficulties of Bonnie Post, the O'Brien siblings' mother, during marital proceedings, VanVechten and the Bank approved of income distributions of $2,000.00 on behalf of each O'Brien sibling (Pet. Ex. 7, 11; GAL Ex. 3-5, 8). Consequently, VanVechten and the Bank made similar income distributions of $2,000.00 on behalf of Eva Breneman, Reed Breneman, Aaron Kielhack and Sarah Kielhack — decedent's four other great-grandchildren alive at that time (Pet. Ex. 8-12; GAL Ex. 6-8). In 1979 and 1980, the only income distributions made were for the benefit of Reed ($2,350.00) and Eva Breneman ($1,375.00) toward their primary school education in Singapore (Pet. Ex. 15, 16, 18-21; GAL Ex. 13-21). Notably, these were the only income distributions made for primary school education costs during the accounting period.

While no income distributions were made in 1981 (Pet. Ex. 1 — Sch. D-1), each year from 1982 through March 1999, income distributions, totaling $921,173.32, were made to or for the benefit of 10 great-grandchildren toward tuition and/or attendant costs (i.e., housing, meals, student activities, etc.) for preparatory ("prep") school and/or college, to wit (Pet. Ex. 1 — Sch. D-1):

Issue of Ella Place (i.e. O'Brien siblings) — $439,685.17, as follows: Stephen received $117,787.32 from 1982 to 1991 (Pet. Ex. 28-30, 35, 43, 46, 55, 56, 59, 60, 76-79, 81, 86, 103-105, 109, 110, 111); Lauren received $112,995.72 from 1985 to 1992 (Pet. Ex. 28, 36, 37, 42, 45, 57, 70, 70B, 73, 84, 85, 89, 90, 95-98, 100, 111, 119); and Chrystie received $208,902.13 from 1988 to 1997 (Pet. Ex. 48-51, 58, 71-73, 75, 86, 87, 92, 93, 101, 102, 105, 106, 127, 130-132, 135, 154-157, 170-173; GAL Ex. 43);

Issue of Sally Cross — $481,488.15, as follows: Eva Breneman received $68,915.00 from 1986 to 1991 (Pet. Ex. 23-25, 35A, 39-41, 44, 63-65, 94, 107, 112); Reed Breneman received $120,458.87 from 1989 to 1996 (Pet. Ex. 61, 68, 79, 83, 113,140, 141); Aaron Kielhack received $75,927.28 from 1989 to 1993 (Pet. Ex. 62, 62A, 67); Sarah Kielhack received $77,045.00 from 1991 to 1995 (Pet. Ex. 132, 133); Douglas Kingham received $85,162.00 from 1993 to 1999 (Pet. Ex. 125, 137, 141, 142, 171-173, 177-180); James Kingham received $52,110.00 from 1995 to 1998 (Pet. Ex. 137, 141, 142, 174, 175); and Campbell Cross received $1,870.00 in 1999.

No income distributions were made to or for the benefit of any issue of Ann Beck during the entire accounting period (Pet. Ex. 1 — Sch. D-1).

Also, throughout the accounting period, VanVechten and petitioners (collectively "the co-trustees") took annual principal and income commissions on a quarterly basis. In this respect, paid commissions charged to principal total $406,523.86, with $56,909.57 paid to VanVechten, $260,104.16 paid to the Bank, and $89,510.13 paid to Downey (Pet. Ex. 1 — Sch. C), while paid commissions charged to income total $302,921.84, with $56,909.57 paid to VanVechten, $191,799.90 paid to the Bank, and $54,212.37 paid to Downey (Pet. Ex. 1 — Sch. C-2). Also, the account shows a total of $40,274.09 in unpaid principal paying commissions sought, pursuant to SCPA 2309(1) and/or SCPA 2312(4)(a), by VanVechten ($6,511.19 [Dec. 26, 1976 — Jan. 1, 1991]), Downey ($10,423.66 [Jan. 18, 1991 — March 31, 1999]), and the Bank ($23,339.24 [Dec. 26, 1976 — Mar. 31, 1999]) (Pet. Ex. 1 — Sch. C-1, H). However, despite the fact that, except for 1979, income distributions were made each year from 1977 through 1999 to or for the benefit of at least one great-grandchild, the co-trustees failed to provide annual statements to any great-grandchild or their parents, as required by SCPA 2309(4) and 2312(6), until 1998.

Additionally, the co-trustees paid fiduciary income taxes of $1,293,093.58 chargeable to principal (New York — $305,243.90; Federal — $987,849.68) and $141,799.34 chargeable to income (New York — $40,390.35; Federal — $101,408.99) (Pet Ex. 1 — Sch. C, C-2).

The Instant Proceeding and Objections

On February 1, 2000, petitioners commenced the instant proceeding to judicially settle their intermediate account as co-trustees, which also encompasses the final account of VanVechten's proceedings as a co-trustee through January 7, 1991. The seven adult objectants — all of whom are members of the Place family — and the GAL (collectively "objectants") allege that the co-trustees abused their discretion and/or breached their fiduciary duty to them in several respects. They further allege that the co-trustees should be surcharged for retaining annual commissions without furnishing the annual statement(s) required by SCPA 2309(4) and 2312(6), and that the Bank should be surcharged for retaining commissions exceeding the minimum compensation awardable under SCPA 2312. In addition, certain objectants challenge the amount of $50,000.00 in counsel fees sought by the law firm of Stroock Stroock & Lavan, LLP ("Stroock firm" [Pet. Ex. 1 — Sch. C-1]) and/or seek removal of petitioners from office. Finally, although unpleaded, objectants allege that the Bank was disqualified to serve as a trustee at the end of the accounting period, due to its 1999 felony conviction under Federal law, and that its failure to inform them of this conviction is grounds for surcharge and/or removal.

At trial, Downey and John P. Genn, III ("Genn"), the Bank's administrative officer for the Trust from November 1998 through the end of accounting period, testified on petitioners' behalf. Petitioners also offered pre-trial examination transcripts of: (i) William J. Wilkie ("Wilkie"), an employee of the Bank for 43 years who was unavailable to testify at trial for medical reasons (Pet. Ex. 196); (ii) Norman C. Cross, Jr., a grandson of decedent (Pet. Ex. 197); and (iii) Ralph P. M. Beck, also a grandson of decedent (Pet. Ex. 196). Stephen and Lauren, as well as Lauren Young, mother of John and Brittany Young, and David L. Place, father of Zachary Place, testified on objectants' behalf. Objectants' also offered the pre-trial examination transcript of Eva Breneman (GAL Ex. 49).

APPLICABLE LAW AND CONCLUSIONS

It is well settled that in a contested accounting proceeding, this court has the power to initiate an inquiry into all pertinent items of the account before approving them (Matter of Stortecky v. Mazzone, 85 NY2d 518 [1995]; Matter of Hawwa A., 9 AD3d 362 [2004]). Upon reviewing the account and hearing the parties' proof, SCPA 2211(1) grants this court broad discretion to make "such order or decree as justice shall require" (Matter of Acker, 128 AD2d 867 [1987]). Applying the foregoing rule upon a finding of misfeasance by a fiduciary, the court may fashion any remedy it deems necessary to redress a successful objectant, including, but not limited to: (i) surcharge; (ii) denial of all or some commissions; and (iii) imposing interest on a surcharge. When it is warranted, the court may impose all of the foregoing remedies (Matter of Kaskawits, 25 Misc 3d 1228[A], 2009 NY Slip Op 52317[U] [2009]).

The Bank's Felony Conviction

Although not originally pleaded in any objections filed, objectants contend that the Bank should be surcharged or denied commissions and/or removed as trustee for continuing to act as a fiduciary after it was named, in March 1999, in a federal felony information and pleaded guilty, in July 1999, to three counts of unlawful diversion of unclaimed funds (see 18 USC §§1005, 2). Initially, in view of the thorough treatment the parties' have given this issue in their post-trial submissions, the court will deem all objections to be amended to include the foregoing allegations (CPLR 3025[c]; see AVR Acquisition Corp. v. Schorr Bros. Develop. Corp., 270 AD2d 372 [2000]). However, the court disagrees with objectants' contention, and denies their requests for relief against the Bank. Although the court could have removed the Bank as co-trustee of the Trust on the basis of its felony convictions (see SCPA 719[6]), whether to do so is discretionary with the court (Matter of Tissot, NYLJ, Aug. 27, 1997, at 24, col. 5 [Sur Ct, Nassau]). Generally, the test is whether the conduct for which the fiduciary has been convicted is deemed to endanger the estate or trust or seriously impede the administration thereof (Matter of Strickland, NYLJ, July 23, 2001, at 36, col. 5 [Sur Ct, Suffolk]; Matter of Tissot, supra; see also Matter of Braloff, 3 AD2d 912 [1957], affd 4 NY2d 847 [1958]).

Here, the court finds that surcharge and/or denial of commissions is not warranted. The Bank was not a convicted felon until its sentencing on July 26, 1999 — after the final date of its account in this proceeding. Further, on December 2, 1999, less than six months after its conviction, New York State issued a certificate of relief from disabilities, specifically relieving the Bank of "forfeitures, disabilities, or bars" under SCPA 707(1)(d) (Pet. Ex. 191). Additionally, by order dated May 19, 2000, the Supreme Court, New York County granted the Bank's application pursuant to Banking Law §154, seeking to substitute its affiliate, Bankers Trust Company of New York, in its place to administer its fiduciary accounts (Pet. Ex. 190, 192).

Abuse of Discretion / Breach of Duty Objectants' numerous allegations of the co-trustees' breach of fiduciary duty and/or abuse of discretion can be summarized as follows: Abuse of Discretion : (i) the co-trustees operated the Trust in an "arbitrary and capricious" manner and/or "without any set plan of administration", especially when they stopped making "sprinkle" payments of any income after 1978 (Objections — Lauren/Chrystie & GAL: # 3; Objections — Stephen: # 8); (ii) the co-trustees refused to honor some reasonable requests for income distributions for educational purposes by narrowly interpreting Article I(A) of the Trust to limit distributions solely for prep school and/or college costs, and they misconstrued decedent's intent with regard to "equality of payments" (Objections — Lauren/Chrystie & GAL: # 1; Objections — Stephen: # 2); and (iii) the co-trustees denied all reasonable requests for distributions of principal under the "accident/illness/emergency" provisions of Article I(B) of the Trust, particularly Stephen's request attendant to his 1994 auto accident, Lauren Young's 1997 request attendant to severe burns sustained by Brittany, and Bonnie Post's 1998 request attendant to certain medical issues Chrystie had incurred (Objections — Lauren/Chrystie & Objections — GAL: # 2; Objections — Stephen: # 3). Breach of Duty : (i) the co-trustees improperly assessed the requests of different beneficiaries by "disparate standards", especially by favoring members of the Cross family over members of the Place family (Objections — Lauren/Chrystie & GAL: # 6; Objections — Stephen: # 9); and (ii) the co-trustees retained excessive income, thereby generating unnecessary Federal and New York state fiduciary income taxes and improperly increasing their commission base, instead of making income distributions (Objections — Lauren/Chrystie & Objections — GAL: # 4, 10; Objections — Stephen: # 1, 5, 11).

Abuse of Discretion - A party who alleges that a trustee has abused its absolute discretion with respect to requests for trust invasions bears the burden of proving such abuse of discretion (see Matter of Snow, 136 Misc 771 [1930], affd 232 App Div 655 [1931]). In such circumstances, "[t]o determine whether a trustee's distribution of trust assets was proper, the settlor's intent controls," as determined from the unambiguous language of the trust instrument itself (Matter of Wallens, 9 NY3d 117, 122 [2007]; see Matter of Chase Manhattan Bank, 6 NY3d 456 [2006]; Matter of Flyer, 23 NY2d 579, 584 [1969]; Matter of Stillman, 107 Misc 2d 102, 105 [1980]). A court will not interfere with the trustee's actions unless the trustee, in exercising or failing to exercise the stated discretionary power, has acted: (i) dishonestly; or (ii) with an improper, even though not dishonest, motive; or (iii) beyond the bounds of reasonable judgment; or (iv) in a manner where the trustee has failed to use its judgment (Restatement [Second] of Trusts §187, comment e; see Matter of Stillman, 107 Misc2d at 110; see also Matter of Sanders, 158 Misc 2d 606, 608 [1991]; Matter of Carter, 15 Misc 2d 599, 601 [1958]; Matter of Riddle, NYLJ, Nov. 21, 1994, at 29, col. 6 [Sur Ct, New York]). In the instant case, the court concludes that the record is devoid of any evidence that the co-trustees acted dishonestly, or with an improper motive, or beyond the bounds of reasonable judgment, or in a manner where they failed to use their judgment in any respect in administering the Trust during the accounting period (Restatement [Second] of Trusts §187, comment e; Matter of Stillman, 107 Misc 2d at 110). Specifically, Genn testified that the Bank's general procedure for handling a request for distribution was as follows: (i) if necessary, the administrative officer would request additional financial information and/or documents in support of the request from the beneficiary requesting the distribution; (ii) the administrative officer would prepare an in-house memorandum, which usually included a summary of the Trust's history, its value and estimated income, previous distributions, the pertinent trust provisions, and a recommendation on the request; and (iii) the Bank's Discretionary Payments Group ("DPG"), comprised of three senior trust department members, would review the memorandum and determine whether to grant, modify, or deny the requested distribution (PTT — T: 84-87, 115-118, 149-150, 351-352, 416; T: 333-337). Downey would routinely consult with the Bank on all matters affecting the Trust, and would usually refer to the Bank any requests for distributions by or on behalf of any great-grandchildren (T: 96-97). As to the Trust's creation, according to Downey, decedent intended to ensure that each of his great-grandchildren would have a "chance at a good education" and receive "a substantial lump sum gift" after all of them had been properly educated (Pet. Ex. 4; T: 93-94). From the Trust's creation, consistent with decedent's intentions and the terms of Article I(A), the Bank and VanVechten adopted a "policy" to administer the Trust to produce sufficient income to provide to any great-grandchild the opportunity to attend prep school and college. This policy, of which Downey was fully aware from its inception, did not include distributions for primary or secondary school education otherwise available through public school systems, where appropriate (Pet. Ex. 4; T: 77-80, 85-86). In implementing this policy, the record reflects that the co-trustees consistently monitored the Trust's portfolio to ensure the availability of sufficient income to pay for prep school and college costs for any great-grandchild who reached that level of education during the accounting period (Pet. Ex. 13, 15, 32, 38, 90, 129, 136, 146, 148, 169, 176). It further reflects that, after August 1995, petitioners retained / invested excess income and, ultimately, created the accumulated income account to ensure that income was readily available not only for those great-grandchildren in prep school or college at that time but also for the benefit of those great-grandchildren who would be attending prep school and/or college prospectively (Pet. Ex. 136, 182; GAL Ex. 38, 40, 41, 44). In reviewing the co-trustees' distributions of income, the record reflects that before any great-grandchildren were old enough to attend prep school or college, $2,000.00 was distributed for the benefit of each great-grandchild alive at that time, including the three O'Brien siblings (Pet. Ex. 7-12; GAL Ex. 3-8). Also, the only income distributions made during the entire accounting period for primary school education costs ($3,725.00) were made in 1979 and 1980 for the benefit of two Cross great-grandchildren living in Singapore at that time (Pet. Ex. 15, 16, 18 — 21; GAL Ex. 13-21). Again, these distributions were made before any great-grandchildren had reached prep school age.

The record further reflects that, prior to VanVechten's death, the co-trustees denied only two requests for income distributions pertaining to educational purposes, to wit: (i) in 1998 and 1989, requests for $8,000.00 in costs attendant to an educational camp Chrystie had attended each summer were denied because Chrystie was not yet officially enrolled in prep school or college when she attended those camps (Pet. Ex. 52-55, 69); and (ii) Stephen's 1989 request for the tuition balance ($1,920.00) attendant to a summer school class abroad was denied, since the "demands on the [T]rust" at that time mitigated against payment of costs for summer school programs (Pet. Ex. 76, 77). Subsequently, petitioners denied Chrystie's 1995 request to have the Trust pay any taxes incurred on the Trust income applied for her benefit, on the basis that it was the beneficiary's personal responsibility to pay such taxes (Pet. Ex. 130, 131, 134, 135). Thus, on all applicable occasions, the co-trustees acted consistently with their policy in administering the Trust, and neither Chrystie nor Stephen can claim any prejudice or harm from the foregoing decisions, given the significant amounts of Trust income each received toward their respective prep school and college educations during the accounting period (Pet. Ex. 1 — Sch. D-1). The record also establishes that in November 1991, Lauren Young made a request for reimbursement of pre-school tuition ($3,000.00) on behalf of her son, John Young (Pet. Ex. 5; GAL Ex. 26), and David L. Place made a request for an income distribution of $2,500.00 per month for the benefit of Zachary Place on account of their family's financial difficulties at that time (GAL Ex. 28). In January 1992, after discussions with the Bank's officials (Pet. Ex. 6; GAL Ex. 23), Downey sent an "introductory" letter to all great-grandchildren of decedent, copying their parents and grandparents (Pet. Ex. 4, 114). Therein, he carefully explained the Trust's genesis and the co-trustees' policy of limiting any distributions of income therefrom for prep school and college, and reiterated the financial reasons for not permitting income distributions for costs attendant to pre-school or primary school prospectively, as many great-grandchildren were fast approaching prep school and/or college attendance at that time (Pet. Ex. 4, 114; SOB Ex. 10; GAL Ex. 31). From 1992 through 1995, Downey received several inquiries from or on behalf of Place and Cross great-grandchildren as to the prospective use of Trust income and/or the implementation of a "policy" for post-college education purposes, including law school (Pet. Ex. 115, 122, 124, 138; GAL Ex. 34). After extensive internal discussions about the viability of these requests and the Trust's prospective ability to continue to provide prep school and college educations to those great-grandchildren who had yet to attain prep school age (Pet. Ex. 118, 121, 123, 126, 143; GAL Ex. 32, 36), petitioners declined to alter their existing policy until a post-college education scenario actually arose (Pet. Ex. 124, 144). In September 1997, a request was made for annual income distributions from the Trust of $10,000.00 each to six Place great-grandchildren, including the O'Brien siblings, Zachary Place, and David M. Place (Pet. Ex. 152, 159-161; SOB Ex. 28, 29). In response, Downey again wrote to all great-grandchildren, copying their parents and grandparents, in which he described the financial status of the Trust at that time (i.e., market value in excess of $5.4 million, producing $125,000.00 in income annually), and projected that as many as eight great-grandchildren were going to need Trust income for prep school and/or college costs from 2004 through 2011 (Pet. Ex. 162; SOB Ex. 7). In sum, Downey reiterated the enforcement of the existing policy, "[w]ithout ruling out a possible change of policy in the future" (Pet. Ex. 162; SOB Ex. 7). Clearly, the record establishes that the co-trustees administered the Trust well within the parameters of the language in Article I(A). More particularly, once Stephen — the eldest great-grandchild — was old enough to attend prep school, the co-trustees not only implemented their policy of limiting income distributions to prep school and college costs consistently, but also adhered to a standard process in gathering information and reviewing the applicable circumstances under which each request for distribution was made (see Restatement [Second] of Trusts §187, comment h). Accordingly, to the extent that the objectants allege that the co-trustees' denials of any requests for distributions were "arbitrary and capricious" and/or that they operated the Trust "without any set plan of administration," their objections are dismissed. For similar reasons, Stephen's request for a construction of the Trust instrument to direct petitioners to pay income for purposes other than prep school and/or college costs is also denied. As to petitioners' rejection of requests for principal distributions under the "accident/illness/emergency" provision of Article I(B), the record reflects that on the three occasions cited in the parties' objections, petitioners acted well within the bounds of their discretion in denying principal distributions from the Trust. Specifically, in April 1994, Stephen requested a distribution of $7,434.00 from the Trust to cover medical expenses he had sustained in a one-car accident three months earlier (Pet. Ex. 128; SOB Ex. 11). At the Place Trust trial, Stephen did not recall if he ever received a response his request (PTT-T: 627-628). Three years later, he requested that petitioners distribute $7,070.10 to him from the Trust "for payment of medical expenses" in connection with his 1994 accident. Petitioners rejected this request (SOB Ex. 25, 30). In October 1997, Jonathan Manny Place, Stephen's uncle ("Jonathan"), contacted the Bank on Stephen's behalf and requested $12,000.00 from the Trust for various expenses Stephen had incurred as a result of his 1994 accident, including $3,415.00 in unpaid medical bills (SOB Ex. 19). On October 23, 1997, the Bank informed Jonathan that, in light of the co-trustee's policy of using the Trust solely for educational purposes, it would consider Stephen's request under the Place Trust, rather than the Trust (SOB — Ex. 26). In November 1997, the Bank approved a distribution to Stephen of $3,415.00 from the Place Trust for "out of pocket" medical expenses, but denied reimbursement for other expenses, citing Stephen's failure to maintain proper insurance to cover those other expenses at the time they were incurred (SOB Ex. 30, 31). Similarly, the requests made on behalf of objectants Brittany and Chrystie, respectively, although initially presented to petitioners, were ultimately reviewed by the Bank as sole trustee of the Place Trust, and, thereupon, partial distributions were made as follows: (i) in July 1997, the Bank approved of a $13,740.00 payment to Lauren Young, covering all requested expenses incurred in connection with Brittany's burn accident, except for lost wages ($5,525.00) and an unnamed miscellaneous expense ($235.00) (PTT-Pet. Ex. 68, 69); and (ii) in July 1998, the Bank approved of $4,259.00 for legal fees attendant to Bonnie Post becoming guardian for Chrystie and $5,377.00 for expenses incurred during Chrystie's hospitalization, while rejecting payment of $2,367.00 for unspecified items deemed "inappropriate" (GAL Ex. 33; PTT — Pet. Ex. 93).

In short, objectants have failed to establish that petitioners' denial of the subject requests for principal distributions under the Trust's "accident/illness/emergency" provisions prejudiced them in any way, and they have failed to submit any evidence in support of their claim that these transactions amounted to an abuse of discretion by petitioners in their administration of the Trust (see Matter of Winston, 39 AD3d 765 [2007]; Matter of Holstein, 38 AD3d 1333 [2007]). Accordingly, Objections — Lauren/Chrystie and Objections — GAL: # 1, 2, and 3, and Objections — Stephen: # 2, 3 and 8 are hereby dismissed.

Breach of Fiduciary Duty

It is well settled that "'a fiduciary owes a duty of undivided and undiluted loyalty to those whose interests the fiduciary is to protect.' * * * 'This is a sensitive and "inflexible rule of fidelity, barring not only blatant self-dealing, but also requiring avoidance of situations in which a fiduciary's personal interest possibly conflicts with the interest of those owed a fiduciary duty'" (Matter of Wallens, 9 NY3d at 122, quoting Birnbaum v. Birnbaum, 73 NY2d 461, 466 [1989]; see Matter of Rothko, 43 NY2d 305 [1977]; Matter of Gould, NYLJ, Oct. 21, 2002, at 26, col. 6 [Sur Ct, Nassau]). Additionally, a trustee has a duty to administer a trust in a manner that is impartial with respect to the various beneficiaries of the trust, requiring that: (a) in investing, protecting and distributing the trust estate, and in other administrative functions, the trustee must act impartially, with due regard for the diverse beneficial interests created by the terms of the trust; and (b) in consulting and otherwise communicating with beneficiaries, the trustee must proceed in a manner that fairly reflects the diversity of their concerns and beneficial interests (Restatement [Third] of Trusts §79). The court finds no evidence in the record that the co-trustees breached their fundamental duty of loyalty to objectants by self-dealing. More particularly, objectants' contentions that the co-trustees generated Federal and New York state fiduciary income taxes unnecessarily instead of making distributions to the beneficiaries is wholly unsupported by the record. In this respect, objectants utterly failed to refute petitioners' evidence that any fiduciary taxes incurred and paid from principal ($1,293,093.58) were a result of capital gains generated upon the sale of successful investments. Similarly, objectants failed to establish that any fiduciary taxes incurred and paid from income through August 1995 ($141,799.34) were not the direct result of the co-trustees' compliance with the express directives in Article I(A) of the Trust to retain undistributed income. Also, objectants do not present any evidence to refute petitioners' proof that after August 1995, no additional taxes were incurred and/or paid from income, due to petitioners' investment of any retained income in tax-free vehicles and, ultimately, their establishment and administration of the accumulated income account. To the extent that the objectants allege that the co-trustees gave "preferential treatment" to members of the Cross family regarding income distributions for education, their objections are dismissed. This contention is belied by the fact that, of the nearly $939,000.00 in income distributed during the accounting period, three Place great-grandchildren (i.e., the O'Brien siblings) received only $40,000.00 less than seven Cross great-grandchildren. Moreover, Chrystie received nearly $80,000.00 more than any member of the Cross family, and while all three O'Brien siblings were reimbursed for virtually all of their prep school and college costs, two members of the Cross family — Aaron Kielhack and Sarah Kielhack — received no distributions for their respective education until each attended college (Pet. Ex. 1 — Sch. D-1). Finally, the record is devoid of any additional evidence sustaining this allegation (see Matter of Winston, 39 AD3d 765, supra; Matter of Holstein, 38 AD3d 1333, supra). Accordingly, Objections — Lauren/Chrystie and Objections — GAL: # 4, 6 and 10, and Objections — Stephen: # 1, 5, 9 and 11 are hereby dismissed.

Retained Commissions Without Statements — SCPA 2309(4) and 2312(6)

Objectants contend that the co-trustees should be surcharged and/or forfeit any commissions they retained for the years in which they did not provide annual statements to them in compliance with SCPA 2309(4), SCPA 2312 (6) and/or CPLR 8005 (Objections — Lauren/Chrystie & Objections — GAL: # 5; Objections — Stephen: # 4). In its Decision and Order dated May 28, 2002 (see Matter of Manny, NYLJ, June 10, 2002, at 37, col. 1), this court granted certain objectants' motion for summary judgment, determining that the co-trustees had failed to send out annual statements pursuant to SCPA 2309(4) and/or 2312(6) to all beneficiaries of the Trust entitled thereto, and ordered a hearing on the appropriate surcharge, if any, to be imposed. The facts on this issue are undisputed: (i) the co-trustees took commissions in each year in which such commissions were earned throughout the accounting period; (ii) until 1998, no great-grandchild or his/her parent(s) received annual statements pursuant to SCPA 2309(4) and/or 2312(6); (iii) except for 1981, income distributions were made from the Trust each year to or for the benefit of at least one great-grandchild; and (iv) for 1977 and 1978 and from 1982 through 1997, income distributions were made from the Trust each year to or for the benefit of at least one of the O'Brien siblings, who are the only objectants herein who received income distributions from the Trust prior to 1998. Pursuant to SCPA 2309(4) and 2312(6), an individual and/or corporate trustee, respectively, may retain commissions during the year in which such commissions are earned, provided that such trustee "furnishes annually * * *, to each beneficiary currently receiving income, and to any other beneficiary interested in the income and to any person interested in the principal of the trust who shall make a demand therefor, a statement showing the principal assets on hand on that date, and at least annually or more frequently if the trustee so elects, a statement showing all his receipts of income and principal during the period with respect to which the statement is rendered including the amount of any commissions retained and the basis upon which such commissions were computed." However, as to inter vivos trusts, during the grantor's lifetime, the trustee is required to furnish such statements only to "beneficiaries currently receiving income" (CPLR 8005). Thus, except for 1981, from 1977 until decedent's death in February 1993, the co-trustees were entitled to retain commissions as long as they provided annual statements required by SCPA 2309(4) and/or 2312(6) to any great-grandchild and/or his/her parent(s) on whose behalf income distributions were made (CPLR 8005). However, under the plain language of SCPA 2309(4) and/or 2312(6), the co-trustees improperly took commissions in 1977, 1978, and from 1982 through 1997 because they failed to provide any O'Brien sibling who received income distributions during those years and/or his/her parents with the annual statements required by SCPA 2309(4) and/or 2312(6) in order to take commissions without prior court approval. "In paying commissions to itself without prior court approval, a * * * trustee acts at its peril, since it is subject to liability for interest on commissions improperly taken" (Matter of Hawwa A., 9 AD3d 362, 364, supra). Although it appears that the court has discretion to disregard relatively minor deviations from the statutory requirements (Matter of Collins, 36 AD3d 1191 [2007]), the co-trustees' complete failure to provide any great-grandchild and/or his/her parent(s) with the required annual statements for a 20-year period cannot be considered such a minor deviation. Therefore, the co-trustees — including VanVechten's estate — must pay the Trust statutory interest (i.e., 9 percent per annum) on the commissions improperly taken in 1977, 1978, and from 1982 through 1997 (Matter of Hawwa A., 9 AD3d at 364; Matter of Prankard, 245 AD2d 566 [1997]). Such interest shall be calculated from the respective dates of each such improper commission payment to the date that petitioners' account was filed (i.e., February 1, 2000). Objectants' claim that the co-trustees should forfeit any commissions for those years or any other commissions sought is without merit. Accordingly, Objections — Lauren/Chrystie and Objections — GAL: # 5, and Objections — Stephen: # 4 are sustained to the extent indicated, supra.

Objectants contend that the co-trustees should be surcharged and/or forfeit any commissions they retained for the years in which they did not provide annual statements to them in compliance with SCPA 2309(4), SCPA 2312 (6) and/or CPLR 8005 (Objections — Lauren/Chrystie & Objections — GAL: # 5; Objections — Stephen: # 4). In its Decision and Order dated May 28, 2002 (see Matter of Manny, NYLJ, June 10, 2002, at 37, col. 1), this court granted certain objectants' motion for summary judgment, determining that the co-trustees had failed to send out annual statements pursuant to SCPA 2309(4) and/or 2312(6) to all beneficiaries of the Trust entitled thereto, and ordered a hearing on the appropriate surcharge, if any, to be imposed. The facts on this issue are undisputed: (i) the co-trustees took commissions in each year in which such commissions were earned throughout the accounting period; (ii) until 1998, no great-grandchild or his/her parent(s) received annual statements pursuant to SCPA 2309(4) and/or 2312(6); (iii) except for 1981, income distributions were made from the Trust each year to or for the benefit of at least one great-grandchild; and (iv) for 1977 and 1978 and from 1982 through 1997, income distributions were made from the Trust each year to or for the benefit of at least one of the O'Brien siblings, who are the only objectants herein who received income distributions from the Trust prior to 1998. Pursuant to SCPA 2309(4) and 2312(6), an individual and/or corporate trustee, respectively, may retain commissions during the year in which such commissions are earned, provided that such trustee "furnishes annually * * *, to each beneficiary currently receiving income, and to any other beneficiary interested in the income and to any person interested in the principal of the trust who shall make a demand therefor, a statement showing the principal assets on hand on that date, and at least annually or more frequently if the trustee so elects, a statement showing all his receipts of income and principal during the period with respect to which the statement is rendered including the amount of any commissions retained and the basis upon which such commissions were computed." However, as to inter vivos trusts, during the grantor's lifetime, the trustee is required to furnish such statements only to "beneficiaries currently receiving income" (CPLR 8005). Thus, except for 1981, from 1977 until decedent's death in February 1993, the co-trustees were entitled to retain commissions as long as they provided annual statements required by SCPA 2309(4) and/or 2312(6) to any great-grandchild and/or his/her parent(s) on whose behalf income distributions were made (CPLR 8005). However, under the plain language of SCPA 2309(4) and/or 2312(6), the co-trustees improperly took commissions in 1977, 1978, and from 1982 through 1997 because they failed to provide any O'Brien sibling who received income distributions during those years and/or his/her parents with the annual statements required by SCPA 2309(4) and/or 2312(6) in order to take commissions without prior court approval. "In paying commissions to itself without prior court approval, a * * * trustee acts at its peril, since it is subject to liability for interest on commissions improperly taken" (Matter of Hawwa A., 9 AD3d 362, 364, supra). Although it appears that the court has discretion to disregard relatively minor deviations from the statutory requirements (Matter of Collins, 36 AD3d 1191 [2007]), the co-trustees' complete failure to provide any great-grandchild and/or his/her parent(s) with the required annual statements for a 20-year period cannot be considered such a minor deviation. Therefore, the co-trustees — including VanVechten's estate — must pay the Trust statutory interest (i.e., 9 percent per annum) on the commissions improperly taken in 1977, 1978, and from 1982 through 1997 (Matter of Hawwa A., 9 AD3d at 364; Matter of Prankard, 245 AD2d 566 [1997]). Such interest shall be calculated from the respective dates of each such improper commission payment to the date that petitioners' account was filed (i.e., February 1, 2000). Objectants' claim that the co-trustees should forfeit any commissions for those years or any other commissions sought is without merit. Accordingly, Objections — Lauren/Chrystie and Objections — GAL: # 5, and Objections — Stephen: # 4 are sustained to the extent indicated, supra.

Commissions and Reasonable Compensation — SCPA 2312

Objectants allege that the Bank should be surcharged for taking commissions at the rate allowable to corporate trustees under SCPA 2312, and since they are only entitled to commissions at the rate set forth in SCPA 2309, they have understated the principal and income on hand for the subject accounting period (Objections — Lauren/Chrystie & Objections — GAL: # 7 and 8; Objections — Stephen: # 6 and 10). At both the Place Trial and the subject trial, Genn testified that the Bank provided in-house administrative, investment and tax services in the following manner: (i) as for administrative matters, the Bank was responsible for knowing and carrying out the terms of the Trust, the collection and management of assets, the retention of records, corresponding with counsel in terms of legal issues, corresponding with the beneficiaries; (ii) as for investment matters, the Bank was responsible for identifying appropriate assets in the Trust for sales, raising cash, and ensuring that the trust generated sufficient income for distribution to the beneficiaries; and (iii) as to tax matters, the Bank was responsible for the preparation of annual fiduciary tax returns and tax letters, or K-1 forms, which are provided to beneficiaries for their individual tax liability (PTT-T:183-186, 201-206; T: 334-335, 351). Genn also testified to the Bank's role in retaining and investing excess income and the creation / administration of the retained income account subsequent to August 1995 (T: 358-362). He further testified as to the various rates used by the Bank during the accounting period, as well as the Bank's elimination of a "paying out" commission in 1992 upon its increase in its annual commission rate, and testified that the Bank's corporate commission rates were comparable to those he was familiar with in the industry (PTT-T:178-183, 188-189; T: 339-350, 362-364). Pursuant to SCPA 2312, for trusts with principal exceeding $400,000, a corporate trustee is entitled to "reasonable" commissions, if the trust instrument does not specifically set forth a different rate of compensation, or contains only general language as to commissions allowed by law (SCPA 2312[2]). In reviewing the reasonableness of such commissions charged, absent a surcharge, a corporate trustee is entitled, at a minimum, to compensation equal to that of an individual trustee's commissions under SCPA 2309 (SCPA 2312[4]). In Matter of Prankard (187 Misc 2d 566, 578-579 [2000]), this court determined that in a contested proceeding, when analyzing the "reasonableness" of a corporate trustee's commissions retained pursuant to SCPA 2312, the court should consider the following criteria, where applicable: (1) the size of the trust; (2) the responsibilities involved; (3) the character of the work involved; (4) the results achieved; (5) the knowledge, skill, and judgment required and used; (6) the time and services required; (7) the manner and promptness in performing its duties; (8) any unusual skill or experience of the trustee; (9) the fidelity or disloyalty of the trustee; (10) the amount of risk involved; (11) the custom in the community for allowance to trustees; and (12) any estimate of the trustee of the value of its services (see also Matter of McDonald, 138 Misc 2d 577, 580 [1988]). Additionally, the court should accord appropriate weight to the trustee's published fee rates within its respective marketplace as a significant factor for consideration (Matter of Prankard, 187 Misc.2d at 579). The corporate fiduciary bears the burden to prove its entitlement to commissions retained in excess of the statutory rate (Matter of Prankard, 245 AD2d 566). Applying the foregoing to the facts of this case, the court finds that the Bank has offered sufficient evidence to establish that it is entitled to "reasonable compensation" under SCPA 2312, to wit: (i) the market value of the Trust grew from $1 million to over $7 million during the accounting period; (ii) the Bank's responsibilities, the character of its work, the results achieved, its knowledge, skills and judgment, and the manner and promptness of performing its duties are all amply demonstrated by this record; (iii) the language of Article II(B) of the Trust instrument permits compensation in accordance with the applicable laws in effect during the accounting period; and (iv) the Bank served as a co-trustee from the Trust's inception. Accordingly, Objections — Lauren/Chrystie and Objections — GAL: # 7 and 8, and Objections — Stephen: # 6 and 10 are hereby dismissed. Additionally, although no objection has been made to the Bank's calculation of its commissions, under its discretion to review the entire account, the court concludes that the Bank has improperly calculated its unpaid principal paying commissions. The Bank seeks $23,339.24 in such commissions [Pet. Ex. 1 — Sch. C-1], as calculated in Schedule H of the Account. Based upon its own calculations, however, the court determines that the Bank is entitled to the reduced amount of $7,169.82 in principal paying commissions. Pursuant to SCPA 2312(4)(a), which refers to SCPA 2309(1), the Bank, as a corporate trustee, would ordinarily be entitled to "a commission from principal for paying out all sums of money constituting principal at a rate of [1 percent ]". At trial, however, Genn testified that effective January 1, 1992, the Bank "waived" its principal "paying out" commissions when it increased its annual commission rate at that time (PTT-T:178-183; T: 334-335, 364-366). Thus, the Bank is entitled to commissions of 1 percent of all money paid from principal from the inception of the Trust through December 31, 1991. The court's review of Schedule C of the Account shows that a total of $716,982.43 was paid from Trust principal through December 31, 1991, and 1 percent of that amount is $7,169.82. Notably, the Bank's calculations would result in more than 3.25 percent commissions on the amount paid from principal through December 31, 1991, and more than 1.37 percent commissions on the total amount paid from principal for the entire accounting period. Therefore, the Bank is directed to amend Schedules C-1 and H of the account in accordance with the foregoing determination.

Counsel Fees

Certain objectants have challenged the propriety of the counsel fees sought by the Stroock firm for legal and professional services that firm performed on petitioners' behalf (Objections — Lauren/Chrystie and Objections — GAL: # 9; Objections — Stephen: # 7). In support of the fee application, the Stroock firm has submitted an affidavit of services from Downey, a retired member of the Stroock firm (22 NYCRR 207.45) and attendant time/billing records. These documents indicate that from March 2, 1999 through March 30, 2000, Downey (44 hours, at an hourly rate of $450.00 per hour) and several associates (nearly 148 hours at an average hourly rate of roughly $135.00 per hour) performed numerous legal services attendant to the instant proceeding, including the preparation of the subject account, ascertaining beneficiaries and whether they were adults or infants, and the service and filing of the appropriate papers and documents, billing $37,351.50 in fees. In December 2000, the Stroock firm received a partial payment from the Trust in the sum of $30,000.00 (Downey Aff. of Servs, at 4-5; Ex. B).

It is settled not only that counsel has the burden of establishing the reasonable value of the legal services for which compensation is sought (Matter of Spatt, 32 NY2d 778 [1973]), but also that the Surrogate bears the ultimate responsibility to decide what constitutes reasonable professional compensation in estate and trust matters (Matter of Stortecky v. Mazzone, 85 NY2d 518 [1995]; Matter of Tendler, 12 AD3d 520 [2004]). In determining the reasonableness of the professional fees sought, the court should consider all relevant factors, including: (i) the size of the trust or trusts; (ii) the difficulty of the questions presented; (iii) the skill required to handle the problems presented; (iv) the professional's experience, ability and reputation; (v) the responsibilities involved; and (vi) the benefit resulting to the trust or trusts from the services rendered (see Matter of Freeman, 34 NY2d 1 [1974]; Matter of Potts, 213 App Div 59, affd 241 NY 593 [1968]). Applying the foregoing to the facts of this case, after due consideration of Downey's affirmation of legal services and the time records submitted therewith, the court approves and allows the sum of $37,351.50, as requested, including the $30,000.00 already paid to the Stroock firm, for all legal services rendered through March 30, 2000. The remaining counsel / professional fees charged by the Stroock firm after March 30, 2000 and all other counsel fee applications emanating from the pre-trial litigation and the instant trial shall be evaluated and fixed upon settlement of petitioners' supplemental accounting or pursuant to application(s) made under SCPA 2110. Accordingly, Objections — Lauren/Chrystie and Objections — GAL: # 9, and Objections — Stephen: # 7 are hereby dismissed.

Remaining Contentions

As for certain objectants' contentions that petitioners should be removed based on the court's findings herein, the court denies that application for the reasons set forth, infra, noting that not every misdeed by a fiduciary warrants removal (see Matter of Duke, 87 NY2d 465 [1996]; Matter of Collins, 36 AD3d 1191 [2007]). For similar reasons, any application for punitive damages is hereby denied. The account shall be amended in accordance with the foregoing determination. This proceeding is restored to the court's calendar of Wednesday, August 4, 2010, at 9:30 a.m., for an all-purpose conference after the matter is called that day. Settle decree. 1. Prior to the subject trial, a separate trial occurred in connection with the Bank's intermediate account, covering the period from May 8, 1991 through March 31, 1999, as sole trustee of the Place Trust ("Place Trust trial"). A written decision following that trial was rendered on March 29, 2010. By stipulation of the parties, portions of the transcript and certain exhibits from the Place Trust trial were incorporated into the record of the subject trial, and will be referenced herein by the notation, " PTT ".

{kind=link}

15 comments:

I've been reading about this guy Scarpino. Which mob family does he have ties to?

Judge Anthony Scarpino worked for Bankers Trust Company now owned by Deutsch Bank. There seems to be a CONFLICT here. He is covering for his old employer - CONFLICT = CORRUPTION! But this is not the first time Judge Scarpino has permitted a Felon to be a Fiduciary. The Westchester Guardian published an article about Joseph Pisani, a disbarred attorney, Felon and former State Senator who is a Fiduciary. A Felon can not be a Fiduciary, the law is the law. Judge Scarpino does what he wants and makes it up as he goes along. What over sight is there on this out of control Surrogate (Scarpino). Judge Scarpino is a snakeoil salesman.

WHY, oh, WHY, aren't the FEDS locking up these Judges (THUGS)? What are they waiting for?

Scarpino has had ties to Al Pirro A federal felon (and former husband of the former West DA) since he was a County Judge. Where there is smoke - there is fire. The buzz is that Scarpino is a rat that's why he isn't in jail right now.

How does this animal Scarpino sleep at night?

How does this animal Scarpino sleep at night?

If you had a pension like these ones waiting for you after you retire with the extra bonuses you made ripping the tax payers and destroying families and children. You too can sleep well at night with the help of some xanax to numb your concience if they have any. ----> check out how much your corrupt public servants will get after they retired including the pension corrupt ex senator Bruno is getting http://seethroughny.net

Dear Fed Up

The Feds can no more stop the disgusting pollution of our legal system than BP can stop the oil flowing into the Gulf of Mexico.

God Help the coming generations. They aint got a chance to survive all the filth and greed.

This case should have been a Jury Trial, it wasn't. The reason it wasn't is that the attorneys know that if they insist on a Jury Trial they will be committing professional suicide in Scarpino's Court and any other Surrogate's Court. Without a Jury Trial Judge Scarpino can and does what he wants. I watched him for years and always found him to be extemely Machiavellian in his actions. The fact that Bankers Trust Company-Deutsche Bank are sentenced federal felons and can continue to act as fiduciaries is wrong. The law has decended into the cesspool of corruption and the people charged with being the watch dogs have been bought. Situations like this are the principal reason that I elected to retire.

Tony Scarpino knows where he wants to go from the get go! The fix is in and Machiavellian is an understand statement regarding Tony S.

So fraud wasn't alleged or presumed??

Scarpino is the same dirtbag that screwed the lady that had Cancer. Where is the administrative Judge? If he worked at the bank how can he sit at a trial, that's a conflict.

This is the same Judge that elsewhere on this blog has federal Judges saying that his mtge has the appearance of a bribe. A federa court has made the case, so where is the USAtty?

Sorry for my bad english. Thank you so much for your good post. Your post helped me in my college assignment, If you can provide me more details please email me.

My goal is to formulate my very own activity since you don't see any great jobs available to choose from.

Could any person provide any ideas or sites about how to apply for government grant money to start my personal business? I have been previously looking over the internet but every single website asks for money and I have been previously told by the unemployment office to stay away from the sites that ask for cash for grant related information because they are scammers. I would be sincerely thankful for any support.

Post a Comment