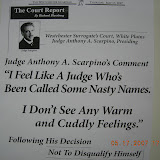

The New York Law Journal by Mark Fass - March 10, 2009

A Brooklyn judge has recused himself from a receivership case where the plaintiff is represented by a law firm that employs two state lawmakers, one of whom voted against a judicial pay raise. In a scathing 10-page decision, Supreme Court Justice Arthur M. Schack (See Profile) wrote that it would be improper for him, as a petitioner in an action against the Legislature seeking raises for judges, to adjudicate an action in which the firm has a stake. "To avoid any potential appearance of impropriety in the instant case, since both Senator Craig M. Johnson and Assembly Member Marc S. Alessi are both of counsel to Jaspan Schelsinger Hoffman . . . I must recuse myself," Justice Schack wrote in JPMorgan Chase v. Bergen Plaza, 126/09. "I hope that Mr. Johnson and Mr. Alessi would allow the judges of this state to receive their first pay raise in this century. Thanks to our legislators . . . our New York State judges are the 'Rodney Dangerfields' of government. A pay raise would help to give us a little respect, instead of, as recently said by Chief Judge Kaye, 'the disdain with which we are treated.'"

Justice Schack's recusal order is yet another salvo in the fight for pay increases for New York's approximately 1,300 trial judges, who have not received a raise since 1999, when the Legislature bumped their salaries to $136,700 a year. No state has gone longer without raising judicial pay; according to one study, New York ranks 48th in judicial pay when adjusted for the cost of living. Last May, then-Chief Judge Judith S. Kaye, a leading advocate for judicial raises, e-mailed the entire state judiciary, advising her fellow judges that they may recuse themselves as a matter of "individual conscience," but that a "strategy" of recusals could "hurt our cause" (NYLJ, May 2, 2008). Two weeks later, the state Commission on Judicial Conduct warned that judges who recuse themselves to protest legislative inaction could face disciplinary actions. The County Judges Association of the State of New York then adopted a resolution supporting "the recusal of any New York State Judges, as a matter of personal conscience, in regard to their ability to be fair and impartial due to the controversy surrounding Judicial compensation." Though no one keeps an official count of the recusals, Steven W. Schlesinger told the Law Journal last year that in a three-month period about 20 judges recused themselves from cases involving his firm. Yesterday, he did not return a call for comment. In one such case, Trump on the Ocean, LLC v. Cortes-Vasquez, 5329-08, then-Nassau Supreme Justice Leonard B. Austin granted a potential intervenor's motion for recusal. "The integrity of the judicial process requires that all attorneys and their clients believe that the decisions of this or any other court are based upon the facts and the law and not some issue in an unrelated matter which can be perceived as affecting the Court's impartiality or sense of fairness," Justice Austin wrote. Last week Justice Austin was appointed to the Appellate Division, Second Department. In the present action before Justice Schack, JPMorgan Chase, the plaintiff, sought the appointment of a receiver for a bankrupt Brooklyn shopping plaza.

Justice Schack recused himself, citing his status as a plaintiff in Maron v. Silver, 06-021984, which seeks an increase in judicial salaries to $169,300. He wrote that it would neither be proper nor appear proper for him to rule on a case involving Jaspan Schlesinger, where both Mr. Johnson and Mr. Alessi are counsel. Mr. Alessi voted against the raises; the issue has not come to a vote before the Assembly. "Both Senator Johnson and Assemblyman Alessi have the right to earn additional income, unlike judges," Justice Schack wrote. "It is high time for [them] to realize that the approximately 1300 New York State judges are working people who deserve their first pay raise in more than a decade." According to a spokesman for the Office of Court Administration, JPMorgan Chase will now go to Justice Abraham Gerges (See Profile), Brooklyn's administrative judge, for reassignment. Antonia Donohue of Jaspan Schlesinger represented the plaintiffs, JPMorgan Chase. She declined to comment. The defendant, Bergen Plaza, did not answer the complaint. Its phone has been disconnected and no one responded to an e-mail requesting comment. The judges' pay-raise suit, Maron, is not faring well. In December 2007, Albany Supreme Court Justice Thomas J. McNamara (See Profile) dismissed all but one claim (NYLJ, Dec. 3, 2007). The Appellate Division, Third Department, affirmed 4-1, and the judges are now seeking leave to appeal (NYLJ, Nov. 14, 2008). There are two other lawsuits seeking higher pay for judges. Larabee v. Silver, 112301/07, was filed in Manhattan Supreme Court in September 2007 on behalf of the New York City Family Court Association, the state Family Court Judges Association, the New York City Civil Court Judges Association and the New York City Criminal Court Judges Association. In Kaye v. Silver, 400763/08, filed in April 2008, Judge Kaye claimed the Legislature denied the judges their constitutional right to an adequate salary. Manhattan Supreme Court Justice Edward Lehner is now considering a motion for summary judgment and a motion to dismiss in Kaye. Justice Lehner's denial of the government's motion for summary judgment in Larabee has been appealed to the Appellate Division, First Department. Mark.Fass@incisivemedia.com

**********

A ‘Little Judge’ Who Rejects Foreclosures, Brooklyn Style

The New York Times by MICHAEL POWELL - August 31, 2009

The judge waves you into his chambers in the State Supreme Court building in Brooklyn, past the caveat taped to his wall — “Be sure brain in gear before engaging mouth” — and into his inner office, where foreclosure motions are piled high enough to form a minor Alpine chain. Every week, the nation’s mightiest banks come to his court seeking to take the homes of New Yorkers who cannot pay their mortgages. And nearly as often, the judge says, they file foreclosure papers speckled with errors. He plucks out one motion and leafs through: a Deutsche Bank representative signed an affidavit claiming to be the vice president of two different banks. His office was in Kansas City, Mo., but the signature was notarized in Texas. And the bank did not even own the mortgage when it began to foreclose on the homeowner. The judge’s lips pucker as if he had inhaled a pickle; he rejected this one. “I’m a little guy in Brooklyn who doesn’t belong to their country clubs, what can I tell you?” he says, adding a shrug for punctuation. “I won’t accept their comedy of errors.”

The judge, Arthur M. Schack, 64, fashions himself a judicial Don Quixote, tilting at the phalanxes of bankers, foreclosure facilitators and lawyers who file motions by the bale. While national debate focuses on bank bailouts and federal aid for homeowners that has been slow in coming, the hard reckonings of the foreclosure crisis are being made in courts like his, and Justice Schack’s sympathies are clear. He has tossed out 46 of the 102 foreclosure motions that have come before him in the last two years. And his often scathing decisions, peppered with allusions to the Croesus-like wealth of bank presidents, have attracted the respectful attention of judges and lawyers from Florida to Ohio to California. At recent judicial conferences in Chicago and Arizona, several panelists praised his rulings as a possible national model. His opinions, too, have been greeted by a cry of affront from a bank official or two, who say this judge stands in the way of what is rightfully theirs. HSBC bank appealed a recent ruling, saying he had set a “dangerous precedent” by acting as “both judge and jury,” throwing out cases even when homeowners had not responded to foreclosure motions.

Justice Schack, like a handful of state and federal judges, has taken a magnifying glass to the mortgage industry. In the gilded haste of the past decade, bankers handed out millions of mortgages — with terms good, bad and exotically ugly — then repackaged those loans for sale to investors from Connecticut to Singapore. Sloppiness reigned. So many papers have been lost, signatures misplaced and documents dated inaccurately that it is often not clear which bank owns the mortgage. Justice Schack’s take is straightforward, and sends a tremor through some bank suites: If a bank cannot prove ownership, it cannot foreclose. “If you are going to take away someone’s house, everything should be legal and correct,” he said. “I’m a strange guy — I don’t want to put a family on the street unless it’s legitimate.” Justice Schack has small jowls and big black glasses, a thin mustache and not so many hairs combed across his scalp. He has the impish eyes of the high school social studies teacher he once was, aware that something untoward is probably going on at the back of his classroom. He is Brooklyn born and bred, with a master’s degree in history and an office loaded with autographed baseballs and photographs of the Brooklyn Dodgers. His written decisions are a free-associative trip through popular, legal and literary culture, with a sideways glance at the business pages. Confronted with a case in which Deutsche Bank and Goldman Sachs passed a defaulted mortgage back and forth and lost track of the documents, the judge made reference to the film classic “It’s a Wonderful Life” and the evil banker played by Lionel Barrymore. “Lenders should not lose sight,” Justice Schack wrote in that 2007 case, “that they are dealing with humanity, not with Mr. Potter’s ‘rabble’ and ‘cattle.’ Multibillion-dollar corporations must follow the same rules in the foreclosure actions as the local banks, savings and loan associations or credit unions, or else they have become the Mr. Potters of the 21st century.” Last year, he chastised Wells Fargo for filing error-filled papers. “The court,” the judge wrote, “reminds Wells Fargo of Cassius’s advice to Brutus in Act 1, Scene 2 of William Shakespeare’s ‘Julius Caesar’: ‘The fault, dear Brutus, is not in our stars, but in ourselves.’ ”

Then there is a Deutsche Bank case from 2008, the juicy part of which he reads aloud: “The court wonders if the instant foreclosure action is a corporate ‘Kansas City Shuffle,’ a complex confidence game,” he reads. “In the 2006 film ‘Lucky Number Slevin,’ Mr. Goodkat, a hit man played by Bruce Willis, explains: ‘A Kansas City Shuffle is when everybody looks right, you go left.’ ” The banks’ reaction? Justice Schack shrugs. “They probably curse at me,” he says, “but no one is interested in some little judge.” Little drama attends the release of his decisions. Beaten-down homeowners rarely show up to contest foreclosure actions, and the judge scrutinizes the banks’ papers in his chambers. But at legal conferences, judges and lawyers have wondered aloud why more judges do not hold banks to tougher standards. “To the extent that judges examine these papers, they find exactly the same errors that Judge Schack does,” said Katherine M. Porter, a visiting professor at the School of Law at the University of California, Berkeley, and a national expert in consumer credit law. “His rulings are hardly revolutionary; it’s unusual only because we so rarely hold large corporations to the rules.” Banks and the cottage industry of mortgage service companies and foreclosure lawyers also pay rather close attention. A spokeswoman for OneWest Bank acknowledged that an official, confronted with a ream of foreclosure papers, had mistakenly signed for two different banks — just as the Deutsche Bank official did. Deutsche Bank, which declined to let an attorney speak on the record about any of its cases before Justice Schack, e-mailed a PDF of a three-page pamphlet in which it claimed little responsibility for foreclosures, even though the bank’s name is affixed to tens of thousands of such motions. The bank described itself as simply a trustee for investors.

Justice Schack came to his recent prominence by a circuitous path, having worked for 14 years as public school teacher in Brooklyn. He was a union representative and once walked a picket line with his wife, Dilia, who was a teacher, too. All was well until the fiscal crisis of the 1970s. “Why’d I go to law school?” he said. “Thank Mayor Abe Beame, who froze teacher salaries.” He was counsel for the Major League Baseball Players Association in the 1980s and ’90s, when it was on a long winning streak against team owners. “It was the millionaires versus the billionaires,” he says. “After a while, I’m sitting there thinking, ‘He’s making $4 million, he’s making $5 million, and I’m worth about $1.98.’ ” So he dived into a judicial race. He was elected to the Civil Court in 1998 and to the Supreme Court for Brooklyn and Staten Island in 2003. His wife is a Democratic district leader; their daughter, Elaine, is a lawyer and their son, Douglas, a police officer. Justice Schack’s duels with the banks started in 2007 as foreclosures spiked sharply. He saw a plague falling on Brooklyn, particularly its working-class black precincts. “Banks had given out loans structured to fail,” he said. The judge burrowed into property record databases. He found banks without clear title, and a giant foreclosure law firm, Steven J. Baum, representing two sides in a dispute. He noted that Wells Fargo’s chief executive, John G. Stumpf, made more than $11 million in 2007 while the company’s total returns fell 12 percent. “Maybe,” he advised the bank, “counsel should wonder, like the court, if Mr. Stumpf was unjustly enriched at the expense of W.F.’s stockholders.” He was, how to say it, mildly appalled. “I’m a guy from the streets of Brooklyn who happens to become a judge,” he said. “I see a bank giving a $500,000 mortgage on a building worth $300,000 and the interest rate is 20 percent and I ask questions, what can I tell you?”

A ‘Little Judge’ Who Rejects Foreclosures, Brooklyn Style

The New York Times by MICHAEL POWELL - August 31, 2009

The judge waves you into his chambers in the State Supreme Court building in Brooklyn, past the caveat taped to his wall — “Be sure brain in gear before engaging mouth” — and into his inner office, where foreclosure motions are piled high enough to form a minor Alpine chain. Every week, the nation’s mightiest banks come to his court seeking to take the homes of New Yorkers who cannot pay their mortgages. And nearly as often, the judge says, they file foreclosure papers speckled with errors. He plucks out one motion and leafs through: a Deutsche Bank representative signed an affidavit claiming to be the vice president of two different banks. His office was in Kansas City, Mo., but the signature was notarized in Texas. And the bank did not even own the mortgage when it began to foreclose on the homeowner. The judge’s lips pucker as if he had inhaled a pickle; he rejected this one. “I’m a little guy in Brooklyn who doesn’t belong to their country clubs, what can I tell you?” he says, adding a shrug for punctuation. “I won’t accept their comedy of errors.”

The judge, Arthur M. Schack, 64, fashions himself a judicial Don Quixote, tilting at the phalanxes of bankers, foreclosure facilitators and lawyers who file motions by the bale. While national debate focuses on bank bailouts and federal aid for homeowners that has been slow in coming, the hard reckonings of the foreclosure crisis are being made in courts like his, and Justice Schack’s sympathies are clear. He has tossed out 46 of the 102 foreclosure motions that have come before him in the last two years. And his often scathing decisions, peppered with allusions to the Croesus-like wealth of bank presidents, have attracted the respectful attention of judges and lawyers from Florida to Ohio to California. At recent judicial conferences in Chicago and Arizona, several panelists praised his rulings as a possible national model. His opinions, too, have been greeted by a cry of affront from a bank official or two, who say this judge stands in the way of what is rightfully theirs. HSBC bank appealed a recent ruling, saying he had set a “dangerous precedent” by acting as “both judge and jury,” throwing out cases even when homeowners had not responded to foreclosure motions.

Justice Schack, like a handful of state and federal judges, has taken a magnifying glass to the mortgage industry. In the gilded haste of the past decade, bankers handed out millions of mortgages — with terms good, bad and exotically ugly — then repackaged those loans for sale to investors from Connecticut to Singapore. Sloppiness reigned. So many papers have been lost, signatures misplaced and documents dated inaccurately that it is often not clear which bank owns the mortgage. Justice Schack’s take is straightforward, and sends a tremor through some bank suites: If a bank cannot prove ownership, it cannot foreclose. “If you are going to take away someone’s house, everything should be legal and correct,” he said. “I’m a strange guy — I don’t want to put a family on the street unless it’s legitimate.” Justice Schack has small jowls and big black glasses, a thin mustache and not so many hairs combed across his scalp. He has the impish eyes of the high school social studies teacher he once was, aware that something untoward is probably going on at the back of his classroom. He is Brooklyn born and bred, with a master’s degree in history and an office loaded with autographed baseballs and photographs of the Brooklyn Dodgers. His written decisions are a free-associative trip through popular, legal and literary culture, with a sideways glance at the business pages. Confronted with a case in which Deutsche Bank and Goldman Sachs passed a defaulted mortgage back and forth and lost track of the documents, the judge made reference to the film classic “It’s a Wonderful Life” and the evil banker played by Lionel Barrymore. “Lenders should not lose sight,” Justice Schack wrote in that 2007 case, “that they are dealing with humanity, not with Mr. Potter’s ‘rabble’ and ‘cattle.’ Multibillion-dollar corporations must follow the same rules in the foreclosure actions as the local banks, savings and loan associations or credit unions, or else they have become the Mr. Potters of the 21st century.” Last year, he chastised Wells Fargo for filing error-filled papers. “The court,” the judge wrote, “reminds Wells Fargo of Cassius’s advice to Brutus in Act 1, Scene 2 of William Shakespeare’s ‘Julius Caesar’: ‘The fault, dear Brutus, is not in our stars, but in ourselves.’ ”

Then there is a Deutsche Bank case from 2008, the juicy part of which he reads aloud: “The court wonders if the instant foreclosure action is a corporate ‘Kansas City Shuffle,’ a complex confidence game,” he reads. “In the 2006 film ‘Lucky Number Slevin,’ Mr. Goodkat, a hit man played by Bruce Willis, explains: ‘A Kansas City Shuffle is when everybody looks right, you go left.’ ” The banks’ reaction? Justice Schack shrugs. “They probably curse at me,” he says, “but no one is interested in some little judge.” Little drama attends the release of his decisions. Beaten-down homeowners rarely show up to contest foreclosure actions, and the judge scrutinizes the banks’ papers in his chambers. But at legal conferences, judges and lawyers have wondered aloud why more judges do not hold banks to tougher standards. “To the extent that judges examine these papers, they find exactly the same errors that Judge Schack does,” said Katherine M. Porter, a visiting professor at the School of Law at the University of California, Berkeley, and a national expert in consumer credit law. “His rulings are hardly revolutionary; it’s unusual only because we so rarely hold large corporations to the rules.” Banks and the cottage industry of mortgage service companies and foreclosure lawyers also pay rather close attention. A spokeswoman for OneWest Bank acknowledged that an official, confronted with a ream of foreclosure papers, had mistakenly signed for two different banks — just as the Deutsche Bank official did. Deutsche Bank, which declined to let an attorney speak on the record about any of its cases before Justice Schack, e-mailed a PDF of a three-page pamphlet in which it claimed little responsibility for foreclosures, even though the bank’s name is affixed to tens of thousands of such motions. The bank described itself as simply a trustee for investors.

Justice Schack came to his recent prominence by a circuitous path, having worked for 14 years as public school teacher in Brooklyn. He was a union representative and once walked a picket line with his wife, Dilia, who was a teacher, too. All was well until the fiscal crisis of the 1970s. “Why’d I go to law school?” he said. “Thank Mayor Abe Beame, who froze teacher salaries.” He was counsel for the Major League Baseball Players Association in the 1980s and ’90s, when it was on a long winning streak against team owners. “It was the millionaires versus the billionaires,” he says. “After a while, I’m sitting there thinking, ‘He’s making $4 million, he’s making $5 million, and I’m worth about $1.98.’ ” So he dived into a judicial race. He was elected to the Civil Court in 1998 and to the Supreme Court for Brooklyn and Staten Island in 2003. His wife is a Democratic district leader; their daughter, Elaine, is a lawyer and their son, Douglas, a police officer. Justice Schack’s duels with the banks started in 2007 as foreclosures spiked sharply. He saw a plague falling on Brooklyn, particularly its working-class black precincts. “Banks had given out loans structured to fail,” he said. The judge burrowed into property record databases. He found banks without clear title, and a giant foreclosure law firm, Steven J. Baum, representing two sides in a dispute. He noted that Wells Fargo’s chief executive, John G. Stumpf, made more than $11 million in 2007 while the company’s total returns fell 12 percent. “Maybe,” he advised the bank, “counsel should wonder, like the court, if Mr. Stumpf was unjustly enriched at the expense of W.F.’s stockholders.” He was, how to say it, mildly appalled. “I’m a guy from the streets of Brooklyn who happens to become a judge,” he said. “I see a bank giving a $500,000 mortgage on a building worth $300,000 and the interest rate is 20 percent and I ask questions, what can I tell you?”

{kind=link}

10 comments:

And maybe make this judge the CHIEF JUDGE! We need more judges like this!

Why don't we have more judges like Judge Schack?

may recuse themselves as a matter of "individual conscience," but that a "strategy" of recusals could "hurt our cause" (NYLJ, May 2, 2008

explains why my biased judges did not recuse themselves, the ones who tried to selectively & falsely prosecute me........

was I a witness to crimes committed by some judges/sheriffs/lawyers friends,'

yes I was..............

better luck next time bitch!

nice to know you admit you are not judges your are strategizing for your cause!

are the judges recusing themselves because they know each and every case is a set up and they are sick of it............

let's give them a raise, not!

you idiots you are making are honest judges give up with your

Nazi mentality!

hope they get their Summary Trial,

with no right to appeal, make sure the trial alters all information and there are no witnesses or experts or stenographers allowed in the court...........

make sure you set up the jury

paybacks are a bitch Kaye!

or should I say Townsend!

Judges only recuse or disqualify themselves under duress or someone has a gun to their head! This guy sounds like a standup dude. How did he get through the screening by the clerks?

as recently said by Chief Judge Kaye, 'the disdain with which we are treated.'"

she should have just said the people are on to our game

Is Judge Schack aware that Deutsche Bank/Bankers Trust Company is a convicted federal felon? Bet he didn't know that one! SDNY case 99cr250 - 3 felony counts - I say felons don't change, they just keep on their criminal paths - Oh, and when they hit you Judge Schack with their Certificate of Relief from Disabilities be sure to check the date it was issued. Enjoy! LOL

Did anyone see today's NY Post article about a young woman who has had her life wrecked by a wrongful judgment from a debt collector?

Her attorney is suing everyone connected with the debt, but he doesn't seem to ask how the collector got a default judgment against the wrong person?

They had the wrong address and social security number, and got a default judgment against the wrong person.

Aren't court's suppose to dispense Justice? (Just kidding. We all know better.)

I'm sorry for this young woman, but gald that she is not just sitting around quietly.

If the court and judge had done it's job, like the judge here, hopefully this never would have happened to her.

Post a Comment